When your air conditioner stops working, it’s not just uncomfortable — it can be expensive. One of the first things homeowners often wonder is: does homeowners insurance cover AC repairs or replacement? A more accurate question might be: Under what circumstances could your policy help?

When your air conditioner stops working, it’s not just uncomfortable — it can be expensive. One of the first things homeowners often wonder is: does homeowners insurance cover AC repairs or replacement? A more accurate question might be: Under what circumstances could your policy help?

The answer depends on the cause of the damage, the type of unit, and how your policy is written. Understanding when your insurance could help — and when it likely won’t — can save you time, money, and frustration.

Does Homeowners Insurance Cover AC? What You Should Know

How Homeowners Insurance Could Apply to AC Units

Home insurance policies generally divide coverage into two categories that may apply to AC-related damage:

-

Dwelling Coverage: This could apply to built-in systems like central AC units if they are damaged by a covered peril (such as fire or a windstorm).

-

Personal Property Coverage: This may apply to portable or window AC units, depending on the nature of the event and the wording of your policy.

Example:

If a lightning strike damages your central AC, and your policy includes that peril, the cost of repairs could be covered under dwelling protection. If a tree branch crashes through a window and hits a portable AC unit, personal property coverage might come into play.

When Does Homeowners Insurance Cover AC Units?

Homeowners insurance could help with AC repair or replacement, but only under specific conditions. Most policies divide coverage into two relevant categories:

-

Dwelling Coverage: May apply to built-in systems like central AC if damage is caused by a covered peril such as fire, lightning, or a fallen tree.

-

Personal Property Coverage: Might apply to portable AC units if the damage results from a covered event like theft or vandalism.

If your AC unit is built into your home and damaged by a storm, your policy’s dwelling coverage could apply. But if your unit breaks down due to old age, general wear, or lack of maintenance, insurance likely won’t help.

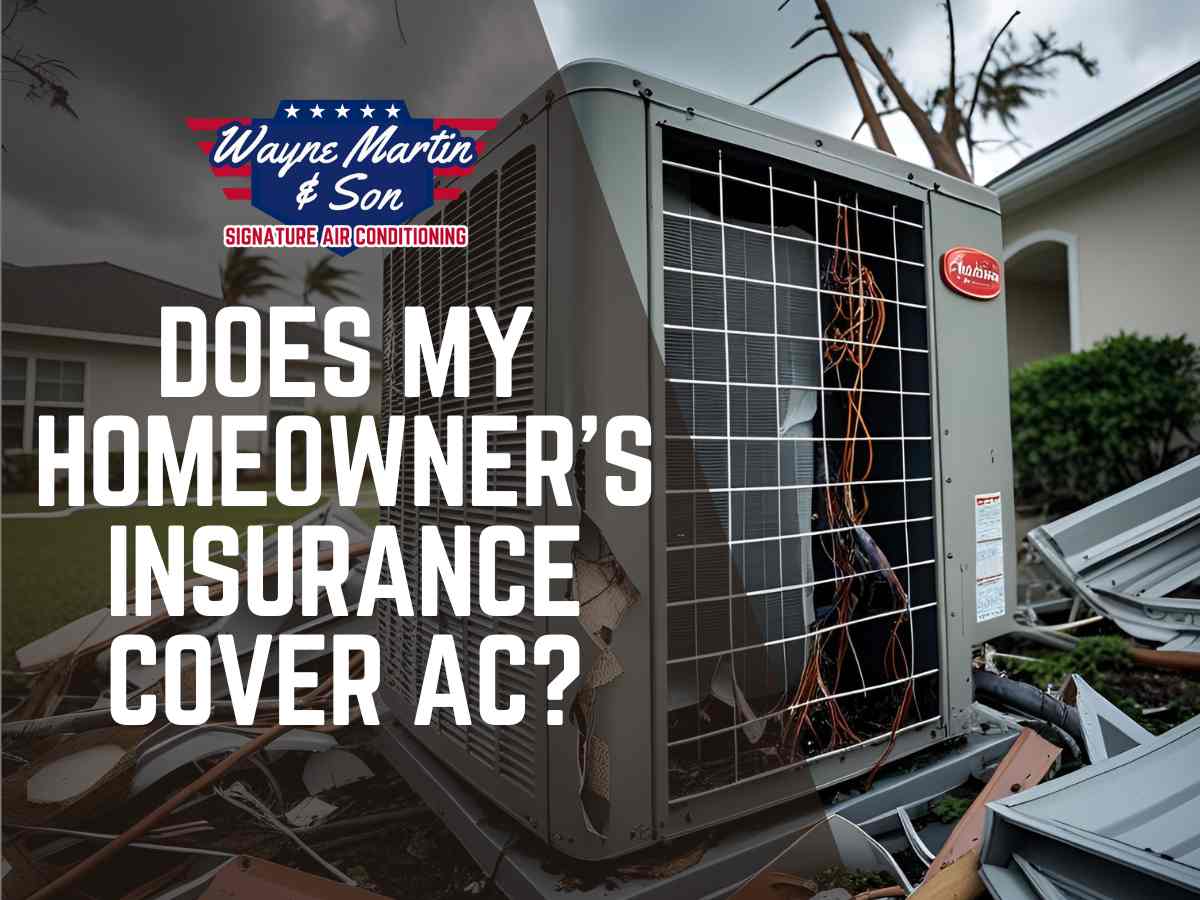

Does Homeowners Insurance Cover AC After Storm Damage?

Yes — but only if the storm is a covered peril in your policy. Lightning strikes, hail, or wind can cause direct damage to an AC unit. In these cases, homeowners insurance could provide coverage for repairs or replacement.

Common storm-related events that may qualify:

-

Lightning frying internal components

-

Hail damaging an outdoor condenser

-

Wind pushing debris into your unit

Always check your policy’s list of named perils or talk to your agent to confirm.

What Types of AC Damage Are Usually Not Covered?

Policies generally exclude coverage for AC issues caused by:

-

Wear and tear from age

-

Lack of routine maintenance

-

Internal mechanical or electrical failures not linked to a covered event

If your AC stops working because the compressor failed or the system is simply outdated, you’ll likely have to pay out of pocket unless you have optional equipment breakdown coverage or a home warranty.

Does Homeowners Insurance Cover AC Theft or Vandalism?

In some cases, yes. If someone steals your outdoor unit or damages it intentionally, your policy’s theft or vandalism coverage could help. You’ll need to file a police report and notify your insurer immediately.

These situations usually fall under named perils, but be aware that deductibles apply — and your reimbursement depends on your policy limits and whether the event meets the definition of a covered claim.

Does Homeowners Insurance Cover AC Replacements?

Replacement coverage may be available, but only if the damage results from a covered peril — not just general failure or wear. For example, if a fire destroys your unit or a tree falls and crushes it, your policy could help replace it, subject to coverage limits and depreciation.

However, if your AC dies on a hot summer day due to a failed compressor or coil, you’ll need to pay for a replacement yourself unless you have extended coverage.

How to Check If Your AC Damage Is Covered

To determine whether your homeowners insurance could cover AC repair, take these steps:

-

Read your declarations page to identify your policy type and coverage areas

-

Look at your named perils list to see which events apply

-

Check for exclusions and limits related to HVAC systems

-

Speak with your insurance agent for a policy-specific explanation

Every policy is different, and even small details — like the type of AC system you own — can affect whether coverage applies.

Preventive Steps to Protect Your AC and Your Wallet

Disclaimer: This article is for informational purposes only. We are not insurance agents or licensed insurance professionals. Always consult your insurance provider or licensed agent for policy-specific advice.